Mexico’s Auto Industry Outlook 2018 – 2024

Warning: foreach() argument must be of type array|object, bool given in /home/mexiconow/public_html/sites/mexiconow/wp-content/themes/mexiconowwpnew/single.php on line 176

The Times They Are A-Changin’

Bob Dylan

Mexico’s auto industry forecast is cautiously optimistic.

After a light vehicle 2017 production record, NAFTA renegotiations, the U.S. new tax law competitiveness hot potato and the exciting presidential election in Mexico blur the horizon.

In spite of a couple of dents to Mexico’s build up of auto assembly capacity, most OEMs with plant projects under development did not blink at the prospect of a NAFTA-less scenario, the potential election of an extreme populist President or higher income tax rates south than north of the border.

The U.S. car and light truck market had a very good year culminating with seven straight years of annual sales growth that ended in 2017 at 17.13 million units sold with a marginal 1.9% loss under 2016, the all-time record year of 17.55 million.

In 2017, Mexico supplied exactly 13.63% of all new light vehicles sold in the U.S., which represents a 75% share of Mexico’s total exports.

The global auto industry has plenty of challenges and opportunities ahead. The major ones are well known: Electric and hybrid vehicles, self-driving cars, app-based transportation services and mass production low-cost models among others.

But few know about the flying-cars, the declining cost of batteries or mobile office-like connectivity. And did you notice the Tesla roadster that was recently launched to space and is now in an orbit between Mars and Jupiter?

The electronics and auto industries are so interrelated that new technology displays and talks dominated the recent Detroit Auto Show; while CES, the Consumer Electronics Show in Las Vegas sported dozens of vehicles. Coincidentally, both events were held back-to-back just this past January.

The Detroit Auto Show is the world’s leader event of its kind. Wondering through the exhibit aisles one can see that it will be a big year for the pick-up market with the return of the Ford Ranger, the tech-loaded Ram 1500 and the redesigned Silverado of GM.

But beyond the shinny vehicles, it was quite interesting to hear OEMs talk about the millions they are going to “lose” in autonomy and electrification R&D.

For example, Ford indicated that US$300 million were spent in mobility and autonomous vehicles development in 2017 and that it would spend US$11 billion through 2022 to introduce and market three dozen battery-electric vehicles and hybrids.

In this article we offer a glimpse of how Mexico’s auto industry may behave in these exciting and revolutionizing times for the sector.

For such a task, we will rely on the voice and opinions of the auto industry leaders in Mexico, most of them pictured in our cover. We are sorry if we missed any of the movers and shakers, they were probably on the road testing self-driving cars and did not make it for our snapshot.

No Place Like Home…

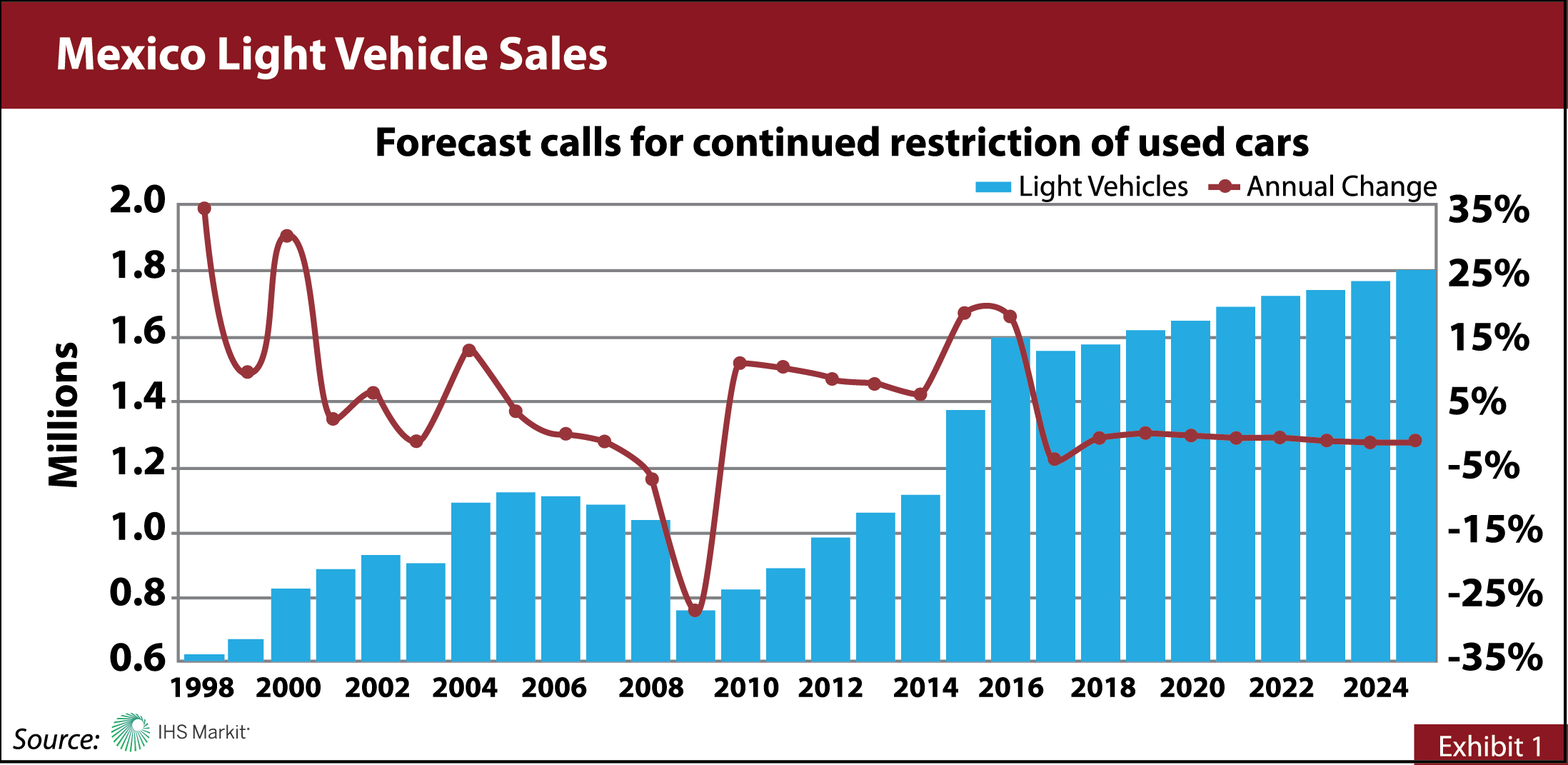

Let’s start our review with the domestic market, which just like the U.S. market also enjoyed 7 years of continuous growth during 2009-2016 and fell -4.6% in 2017 to 1.53 million units sold from the all-time record in 2016 of 1.60 million.

Still, the performance in the 7-year period has been outstanding as the domestic market more than doubled during that time. Please see Exhibit #1 sourced from IHS Markit, a leading auto industry consultant, which shows the historic and forecast data through 2024.

Guillermo Prieto, Executive President of the Mexican Association of Auto Distributors (AMDA) said: “Light vehicles sales rates in Mexico had a 4.6% decrease after having experienced two-digit growth rates over the last two years. There are two causes for this: inflation, which last year escalated to a historic maximum in 17 years, reducing the families' purchasing power, and increasing of the interest rates by the Bank of Mexico, thus slowing down the approval of car-financing credits”.

In Mexico, because of the strict and contained banking loan policies, lending institutions account for only about 25% of new vehicles financing, the big chunk of car loans, about 71%, is provided directly by the OEMs to consumers. Buyers pay in full only 4% of all car purchases.

New car sales were also propelled by the successful and significant reduction of used imported cars. Back in 2006, 2007 and 2008 over one million used units per year in average were brought into Mexico, most of them without complying with environmental regulations.

Through constant and effective lobbying, the auto associations managed to make authorities to enforce the law and curtain import windows. In 2017, only slightly over 120,000 used cars were imported from the U.S.

The IHS market forecast and AMDA agree that going forward, the new auto market will grow at about 2% per year, in line with general economic growth, to possibly reach almost 1.8 million units by 2024.

And as NAFTA continues to be in the Twilight zone, the relevance of production for the domestic market may gain traction among OEMs with plants in Mexico.

Jose Munoz, President of Nissan North America said: “Unlike other assemblers that use Mexico as a factory for exports, we sell a large portion of our production in Mexico. This localization strategy is eliminating the potential negative impact in case the U.S. decided to step out of the North America Free Trade Agreement”.

Nissan produced about 830,000 units in its three plants in Mexico in 2017, and sold 44% of the output in the domestic market capturing a 24% market share, followed by GM in a distant second place at 17%.

But the light vehicle market in Mexico has a lot more potential if certain policies are followed: First and foremost, continuing to control used car imports is evidently a must; second, a new scrappage scheme, aka “Cash for clunkers”, like the one Mexico had back in 2009 with grants of about US$1,000 towards the purchase of a new car is in order again.

Third, lending institutions need to expand their limited burden on car loans, perhaps Mexico’s Banking and Securities Regulator should impose a minimal quota for banks to open more auto credit lines; fourth, OEMs need to design vehicles for the Mexican market, for the Mexican family, today practically all light vehicle models in Mexico have U.S. or global platforms and designs.

And last but not least, fifth, is the need for a fundamental correction: According to the World Bank, Mexico has an economically active population of 59 million; but 60% or 35 million are informal workers, meaning they have no social security, they pay no taxes and lack checking accounts, credit cards and of course, they cannot get a formal loan. Imagine the huge potential domestic market for new cars, if the federal government, perhaps through a tax holiday, would manage to incorporate the informals to the formal economy.

More ideas are welcome to reach, the very reachable domestic market potential of 2 million units well before 2024.

Output and Export Marks

In spite of a slight decrease of 1.9% in the U.S. new light vehicle sales in 2017, Mexico posted a record annual production of 3.77 million units, a record amount of exports at 2.77 million and a record amount of shipments to the U.S. market of 2.34 million; these amounts are 8.9%, 16.7% and 9.4% higher than 2016, respectively.

And 2018 is already looking better than 2017 as during the month of January production was up 4.1% and exports to the U.S. increased 10.1% over the same month in 2017, representing a market share of 15.5% for Mexico in the U.S. new light vehicles market.

Mexico is the #4 global exporter of light vehicles and the #7 in total output as illustrated in Exhibit #2.

As the new assembly plants are launched and their production increases output would be about 4.25 million in 2018 and perhaps even 5 million in just a few years.

The new OEMs in this process include: Audi-San Jose Chiapa (2016), Kia-Monterrey (2016), FCA Compas-Toluca (2018), BMW-San Luis Potosi (2019) and Toyota-Celaya (2021).

But unlike previous years, there is now volatility in Mexico’s auto industry as evidenced by the Ford San Luis Potosi assembly plant sudden termination with the building’s steel structure half way completed and the more recent repositioning of the RAM pick-up from Saltillo to Michigan by Fiat Chrysler.

Sergio Marchionne, Fiat Chrysler Automobiles (FCA) CEO said: “The U.S. is much more pro-business than it has been in a long time. Tax reform (the U.S. cut the corporate income tax rate from 34% to 21%) is going to compensate some of the cost differential in building the vehicle in the U.S. as opposed to building it in Mexico.”

There are many forces influencing auto production in Mexico including: U.S./Mexico politics, the U.S. market sales level, OEMs’ platform strategies, income tax rates, free trade agreements and country and state incentives among others.

As a result, we now have a more ample range of forecasts.

While Mexico’s automotive related associations stay optimistic for the country to reach the 5 million production landmark by 2020 or a few years later, a more conservative forecast from IHS Markit is presented in Exhibit #3 in the context of total North American production, which is expected to be quite stable through the years at about 17.7 million total units.

Notice the subtle changes from 2016 through 2024: Canada and the U.S. each loses 500,000 units while Mexico gains 900,000 representing 26% growth in 8 years and a hair short of reaching 25% output share in North America.

The new facilities that support this production capacity are not transplants of old factories but rather state-of-the-art operations such as the new Audi plant where Industry 4.0 practices are common.

Alfonse Dintner, President of Audi Mexico proudly said: “All manufactured cars are traced during each step of the process. The computer knows the model, features, color and destination of each vehicle and all pieces of equipment are monitored in real time.”

The Inputs

Mexico’s auto-parts industry is ranked #6 in the world, it employs approximately 830,000 workers and has a production output of close to US$85 billion, most of which is exported to the U.S. as shown in Exhibit #4.

Notice that the export value of the auto-parts headed to the U.S. has been about 40% to 50% higher than the value of the light vehicles exported to that market.

Mexico is an auto parts manufacturing powerhouse firing on all cylinders as evidenced by the over 100 new projects and expansions presented in the two- page spread Exhibit #5 in this piece.

The U.S. and Mexico’s auto industries are like Siamese twins, inseparable and highly intertwined.

The supply chains created over the last 50 years are very, very strong and impossible to undo without a huge cost and disruption to the North American automotive production.

Ernesto Hernandez, President of General Motors Mexico underlined: “The integration we have accomplished in over 20 years of NAFTA has been very important for the three countries, and the supply chains that have been developed have an economic value and industrial relations that go beyond any political rhetoric.”

Mexico imports from the U.S. almost US$25 billion worth of auto-parts per year, and most of those are incorporated into finished vehicles that go back to U.S. consumers.

It is estimated that 40% of the value of Mexico made vehicles exported to the U.S. represents auto-parts originally made in the U.S.

Looking inward, Mexico has a problem when dealing with replacement and accessory auto-parts in the aftermarket.

Oscar Albin, Executive President of Mexico’s National Auto Parts Industry Association said: “We have a severe problem related to indiscriminate importation of low value components, particularly from Asia. A lack of proper Mexican quality norms and the lack of technical skills and testing facilities to enforce any norms have allowed entry to all sorts of auto parts. In addition, China offers sub-par parts at very competitive prices, which make it hard for domestic manufacturers to enter the aftermarket. The NAFTA renegotiation talks is a great opportunity to incorporate a special chapter of quality for auto parts for the whole region.”

July 1, 2018

This is a crucial date for Mexico with the presidential elections taking place.

The party in power, President Pena Nieto’s PRI is currently a distant third in the polls battered by multiple waves of corruption. The conservative and divided PAN party is in second place but still about 10 percentage points behind the populist MORENA’s candidate, Manuel Andres Lopez Obrador (AMLO), who is in his third attempt to win the presidency.

The problem with AMLO is his extreme positions such as getting rid of the Energy Reform and cancelling the new Mexico City airport. Although both threats are very hard to implement because of the huge cost of indemnities, just the fact he mentions them is not exactly pro-business.

But carmakers work all over the world, including under totalitarian regimes such China and Russia.

Mayra Gonzalez, President of Nissan Mexico explained: “Mexico’s industry is a global example. Nissan distinguishes itself for working with each administration. Whichever candidate wins the elections; we are going to work side by side with him. We are going to help him to continue consolidating the Mexican auto industry.”

Gabriel Lopez, President and CEO of Ford said: ““Obviously, companies are not invulnerable to the political context of the countries where they operate and the change of administration in the U.S has generated a number of unexpected situations in the U.S-Mexico relation. It has clearly affected the automotive sector, as its weight in the countries’ economies is very meaningful, due to its size and relevance. Consequently, automotive corporations are always a primary interest and demand special attention from politicians”.

The NAFTA Cards

The automotive industry is the main engine of Mexico’s exports. As shown in Exhibit #6, Mexico’s automotive exports generate more foreign income than oil exports, tourism and expatriates’ remittances…together!

The U.S. foreign trade deficit with Mexico in 2017 grew 10.4% from the previous year to reach US$71 billion.

Coincidentally, last year, Mexico’s positive automotive trade balance hurdled over the US$70 billion mark, about 14% higher than 2016.

No wonder the talks to renegotiate NAFTA make progress in most chapters except for the automotive sector, where the U.S. wants to change the rules of origin.

Eduardo Solis, Executive President of the Mexican Automotive Industry Association (AMIA) said: “The United States’ proposition of increasing the regional content for vehicles on NAFTA to 85% –from the current 62.5%- and to set a minimum 50% U.S. parts content is utterly unreachable, even for the industry in the U.S. The industrial leaders in all three countries have an agreement and, clearly, we are going to try to convince the three Governments not to change the origin regulation for the automotive sector, as it has been a fundamental cornerstone for this sector’s success.”

The NAFTA talks may extend beyond the original target date at the end of March. The new projects of many auto firms are in the back burner, but most auto OEMs, with stakes in an advanced stage, hold a resilient stance.

Radek Jelinek, President and CEO of Mercedes Benz Mexico assured: “Regardless of the NAFTA future, Daimler is going to begin producing a model of its Mercedes Benz brand at its plant in Aguascalientes, Mexico, which was built in joint-venture with the Renault-Nissan alliance. We are going to produce models for the U.S. market, primarily”.

Hiroshi Shimizu, President of Honda Mexico expressed: “Honda is maintaining its production in the two plants it has in Mexico, despite the revision to the North America Free Trade Agreement and the car sales deceleration in Mexico’s domestic market. Mexico has an excellent geographical location and we export from here to the U.S, but also to Canada, South America and Europe. Mexico is the second most important market in Latin America for this assembler's operations. It is an important production hub, not only for Honda but also for the automotive industry in general”.

Miguel Barbeyto, President of Mazda Motor Mexico said: “The Japanese assembler Mazda is maintaining its production plans and its operations in Mexico, despite threats of applying customs fees or a border tax to vehicle importation coming from Mexico into the US.”

In theory, without NAFTA, trade rules between the U.S. and Mexico would fall back to World Trade Organization guidelines that would impose a 2.5% U.S. import tax on cars, which is not a showstopper.

Likewise, over 80% of the auto-parts exported to the U.S. would be taxed with 2.5% or less, while the maximum tariff for the rest would be 6%.

But pick-ups and heavy trucks would be smashed with a 25% import duty, and that is not good at all. About 40% of all units exported to the U.S. may fall in this category.

Pick-ups were part of the original “Chicken tax” that dates back to 1963 and originated from a trade dispute between the U.S. and France and Germany.

If push comes to shove, OEMs may shift production to move pick-ups out of Mexico and possibly replace them by units taxed at the lower rate, like Fiat Chrysler already did with the RAM.

Ford does not build pick-ups in Mexico but GM, FCA and Toyota do.

Mayra Gonzalez of Nissan summarized the general feeling among OEMs: “In relation to the NAFTA renegotiation, we have not made any provisions because we don’t know yet what the resolution is going to be. We are open and willing to wait until we receive official information on what these changes are going to be. From there, we would be making any necessary adjustments.”

Still, besides its geographic location next to the U.S. market and its competitive and skilled labor force, Mexico’s cornerstone to promote and lure the global automotive industry has been NAFTA and its web of trade agreements with other countries.

Woo Yeol Park, President of KIA Motors Mexico asserted: “The Pesqueria plant is the seventh plant KIA owns outside of South Korea. It was built in response to the need of having a greater installed capacity in America, where the brand presents double-digit growth rates. We analyzed many different locations and saw that Mexico was the best option. It is part of the NAFTA region and it has Free Trade Agreements with over 40 countries”.

Conclusion

The U.S. trade deficit with Mexico, which is almost seven times smaller than the one it has with China, will not be resolved during or after the NAFTA renegotiation talks, not by the eventual, if any, resulting North American accord.

The U.S. is a huge economy, with tremendous purchasing power by the consumers, businesses and governments, so it is just natural that they would buy more things than consumers of less developed countries would, thus the U.S. has a trade deficit with Mexico.

The overwhelming majority of small and mid-size U.S. firms do not have a marketing presence south of the border, thus the U.S. has a trade deficit with Mexico.

President Trump keeps taunting Mexico, so the peso losses value versus the dollar, making manufacturing costs in Mexico more competitive, thus the U.S. has a trade deficit with Mexico.

U.S. based automotive manufacturers cannot find enough skilled people to fill the thousands of job vacancies available, thus the U.S. has a trade deficit with Mexico.

Mexico is a darn good cost competitive manufacturing platform. What else, other than a trade deficit would a buyer expect to have with a supplier? Thus the U.S. has a trade deficit with Mexico.

The last word goes to Alexander Wehr, President and CEO of BMW Group Mexico: “The NAFTA renegotiation, the opening of new plants, the adaptation of vehicles to the new safety regulations and the challenge of re-activating sales after a period of downfalls are going to define this year for the auto industry in Mexico”.